PDF

PDF ePub

ePub Citation

Citation Print

Print

INTRODUCTION

Following the economic reform in the late 1980s from a centralized economy to a market-oriented economy, the free universal access healthcare system was shifted to a user fee system subsidized by the government. As a result, out-of-pocket expenses for health kept increasing from almost nothing to 65% of the total health expenditure in 1998 and peaked at 72.5% in 2005 (1), pushing many low-income households into financial catastrophe. In 2002, almost 5% of households spent at least 40% of their capacity to pay for healthcare and by 2008 this increased to 17% (1). Also 5.5% of the poorest quintile faced catastrophic expenditure on health in 2002, which rose to 41.8% in 2008 (2, 3, 4, 5, 6). Relying on out-of-pocket financing for health exposes households to potential catastrophic expenditures and creates inequality in access to care. Therefore, the government of Vietnam initiated the Social Health Insurance Program as an active tool to ensure universal coverage of health care. However, although more than two decades has passed, Vietnam has not fully achieved its goal of achieving universal coverage of health insurance.

In this paper, we introduce the development of health insurance in Vietnam emphasizing on barriers to achieve universal coverage. Additionally, based on the facilitating factors to speed-up universal coverage developed by the World Health Organization, concerning specific facilitating factors of Korea, we implement a country-to-country comparison study to answer the question of a possibility to speed-up population coverage of health insurance in Vietnam. Comparison at crucial milestone is focused with current situation of Vietnam and the relevant situation in Korea three decades ago to make indicators comparable. Importantly, the paper examines the applicable lessons from the experience of Korea to Vietnam in achieving universal coverage of health insurance.

THE DEVELOPMENT OF HEALTH INSURANCE IN VIETNAM

The National Health Insurance Program was inaugurated in 1992, following a three-year pilot project of voluntary non-commercial health insurance in the period of 1989-1992. Aiming to contain the growth of out-of-pocket spending, the National Health Insurance program was implemented nationwide, mandating the enrollment of civil servants, employees of state-owned enterprises and any private companies with more than 10 employees, and the pensioners; while other entitlements were under the voluntary scheme (7). Since then, Vietnam has issued a series of laws expanding the portion of mandatory enrollment of health insurance over the population. The Law on Health Insurance in 2008 mandated the enrollment of all the citizens, categorized into 25 groups on individual basis. The "Roadmap" in 2009 to achieve universal coverage under the Law on Health Insurance has made health insurance compulsory for employees of all type of firms (since 2009), students (since 2010), farmers (since 2012), and the self-employed, the dependents and others (since 2014) (8).

Regarding the poor and children-under-six years of age, the Medical Aid Program was established in 2003, in which the government reimbursed directly to healthcare facilities or enrolled them into the National Health Insurance scheme (9, 10). However, since 2008, the Medical Aid program was integrated into the National Health Insurance program. The government did not reimbursed directly to health facilities but instead the government has been paying for the health insurance contributions of these two groups. People of these two groups do not pay co-payment when utilizing healthcare services. Up to now, both compulsory and voluntary schemes co-exist even though the voluntary scheme is to be replaced by compulsory scheme by 2014. The longer the two schemes co-exist, the worse-off for the social health insurance program because of severe adverse selection (11).

At the inauguration of the National Health Insurance Program, it was operated on a multiple fund structure with provincial health insurance funds, which collected revenue and reimbursed for providers within the province, and a national reserve fund (12). In 1998, all the health insurance funds were unified into a single national fund under the administration of the Ministry of Health. In 2003, the Vietnam Social Security (VSS) was established, merging all the existing social insurance schemes including health insurance, pensions, unemployment, and labor insurance. VSS has been the central health insurance pooling entity, whose main responsibility is to collect contributions, contract and reimburse to healthcare providers, pool and manage health insurance fund, and review claims (13). In other words, VSS is the single health insurer in Vietnam. However, in 2008, the Law on Health Insurance decentralized revenue collection and spending at provincial level. Accordingly, each province has a health insurance fund and the national fund managed by VSS has a function of a reserve fund, which balances the deficit and surplus of provincial health insurance funds.

BARRIERS TO ACHIEVING UNIVERSAL COVERAGE IN VIETNAM

Although the Law of Health Insurance was implemented in 2009 and the Roadmap was passed in 2009, the speed of enlarging population coverage has increased insignificantly. In 2010, the number of the insured increased by 1.8% compared to 2009, and had a 3.1% increase in 2011 (MOH, 2013). Such a low speed is due to the following barriers.

Limited ability to afford contributions by a large portion of population

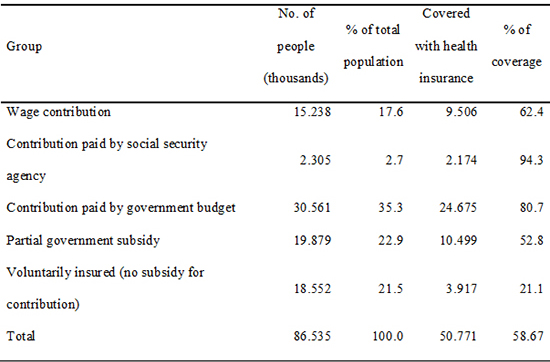

The 25 entitlement groups are classified into four categories based on contribution payment methods: 1) contributions are paid through wage and social allowances, 2) contributions are paid by the government, 3) contributions are shared between the government and individuals, and 4) contributions are paid by individuals. Among those, the government pays contribution for 35.3% of the population (the poor, children-under-six) and supports from 30%-70% of contribution for 22.9% of the population (the near-poor, students). Only half of the third categories are covered with health insurance even though they are partially supported by the government (Table 1). The amount that they have to pay to be insured is still expensive compared to their income because the contribution is calculated based on the minimum salary, not on the ability-to-pay mechanism.

Adverse selection, low benefits, and low quality of services covered by health insurance

Apart from those who have limited ability to afford the contribution, the fourth category (Table 1) is composed of individuals/households who are financially better-off and receive no financial support from the government for their contribution. This category accounts for more than 20% of the population, which is as large as the amount of salary worker. However, only 21.1% of them are insured, and mostly they are insured only when they are sick (14, 15). These people perceive the enrollment contribution as too expensive to justify the expected benefits of insurance coverage (16). Despite of the fact that almost 80% of health services listed in the technical guideline of the Ministry of Health are covered by health insurance, medical services which do not have the exact names as listed would not be reimbursed. Such a technical guideline is not regularly updated, resulting in many services, which are not necessary high-tech services, not being covered by health insurance. In addition, patients do not satisfy with services covered by health insurance receives for low quality of care, long waiting time, and informal payment in the form of gift or cash to health staff (17). These factors militate against the willingness to enroll in National Health Insurance scheme.

Non-comprehensive legal system on health insurance

The legal framework on health insurance in Vietnam has been developed but yet far to be comprehensive. According to the Law, health insurance is managed at provincial level, asking for provincial rules and regulations to operate health insurance based on the Law. However, many provinces do not develop their regulations and guidelines, resulting in loose compliance of enterprises, organization, and individuals regarding health insurance enrollment. Also, the lack of legal and operational guidelines from central government reduces the synchronization of health insurance management nationally.

Low level of computerized administrative infrastructure

Although residents are managed through the identification card and number system, management is heavily manual and has not been computerized. In the health sectors, health services are not coded by number and are not managed through a computer system, which resulted in manual review, payment claiming inaccuracy, and reimbursement delay.

Enrollment fragmentation

Enrollment is on an individual basis and is quite fragmented (12). The dependents are narrowly defined with spouse, parents, and children. However, dependents must live in the same residence with the insured (18). Under the situation of such a weak, non-computerized administrative infrastructure, it is very hard to identify dependents, especially in the informal sectors. Furthermore, additional contributions for the dependents must be paid for them to be insured, making the enrollment of these groups even more difficult.

KOREA'S FACILITATING FACTORS TO SPEED-UP UNIVERSAL COVERAGE

Historically, the transition to universal coverage of health insurance takes many years (Germany, 127 yr; Belgium, 118 yr). However, Carrin argues that the time needed to achieve universal coverage would be shortened (19). Historic review of the World Health Organization on achieving universal coverage outlines facilitating factors to slash the transitional period: economic factor (level of income, structure of economy), demographic factor (distribution of population), social factor (ability to administer), cultural factor (solidarity), and political factor (stewardship) (20). Accordingly, Korea is an "out-standing examples" (21) of achieving universal coverage of health insurance in the shortest period of time in history (20) as a result of a suitable strategy developed based on sufficient conditions of economic development and social characteristics.

The health insurance program in Korea started with the promulgation of workman compensation and a voluntary insurance scheme in 1963. After two years, there were no private enrollers and only two manufacturing companies participating in the scheme. With about six thousand enrollers and high administrative cost, it was impossible for insurers to spread risks sufficiently putting health insurance viability into question (22). Therefore, the Health Insurance Act was amended, starting an era of compulsory health insurance in Korea in 1977 for firms that employed more than 500 employees, extending to firms of 300, 100, and 16 employees in 1979, 1981, 1983, and 1988 respectively. The final expansion was made in 1988 for the rural self-employed and in 1989 for the urban self-employed. It took Korea only 26 yr since Health Insurance Law was passed and only 12 yr since the start of the National Health Insurance program to achieve universal coverage.

Korea developed the National Health Insurance program in a period of high and stable economic growth, bringing greater income for government, enterprises and households, which resulted in a higher capability to contribute to health insurance. Industrialization created more employment in formal sectors and encouraged urbanization, enabling contribution collection and mandatory enrollment enlargement. These advantages created significant facilitating factors for Korea with economic, demographic, social, cultural, and political factors.

CONDITIONS TO SPEED-UP

The development of the National Health Insurance program of Vietnam and Korea is deeply rooted in employment-based insurance schemes. Accordingly, population coverage is expanded through the gradual coverage expansion of the salary workers, then reaching out to the disadvantage population (such as the low income), and eventually approaching the self-employed (24). Therefore, this section presents a comparison of economic, social, and political facilitating factors between the two countries. We believe that it is irrelevant to compare current situation of Vietnam and Korea, therefore, we compare situations of the two countries based on crucial milestones: the inauguration of insurance program (in 1963 for Korea and 1992 for Vietnam) and the starting of compulsory enrolment policy (in 1977 for Korea and 2009 for Vietnam). Sometimes, because of the unavailability of data, indicators of the closest years to the milestones were used.

Similarities: level of income

Economic growth is crucial in implementing national health insurance. A greater level of income increases not only the capability to contribute to prepaid health insurance of enterprises and citizens but also tax revenues for higher government subsidies (20). Korea first introduced health insurance in 1963 when the country was recovering from the Korean War with a GNI per capita of USD 209. The mandatory scheme started in 1977 when the GNI per capita increased to USD 1,012 (25).

The socio-economic crisis in Vietnam in the late 1980s resulted in several health care reforms, including the introduction of national health insurance in 1992 when GNI per capita was USD 200. The Health Insurance Law in 2008 expanded the mandatory scheme of health insurance nationwide when GNI per capita was USD 1,030. Although Vietnam has higher GNI levels at important milestone (Table 2), GNI per capita of the two countries are very similar.

Similarities: ability to administer

Run by the government, a national health insurance program requires sufficiently skilled officers with capacities in book-keeping, banking, and information processing (20). While the introduction and expansion of health insurance nationwide was carried out by political decision, the overall designing and administrating of the program in Korea was delegated to civil servants. Historically, Korea and Vietnam chose civil servants on ability based on national examination and long-term training. Other countries historically appointed civil servants or provided no training mechanism. These days, both Vietnam and Korea have a well-organized local administrative system for the purpose of national security and resident management. Both countries have the resident certificate system where each citizen has an identity number for public administrative related activities, including health insurance management. Moreover, both Korea and Vietnam experienced a period of voluntary health insurance before transferring to the compulsory scheme, equipping basic health insurance related skills for civil servants (25).

Similarities: solidarity

The national health insurance scheme is a cross-subsidized system that requires a certain level of social solidarity so that the better-off are willing to share financial risks with the worse-off (20). Korea is a homogeneous country with only one major ethnic group and a strong sense of nationalism and nation pride. Also, Korea used to be an agriculture country where "unionism" plays an important role in the living environment. Promoting the risk-sharing concept through the message of "sharing the financial burden with those who lack the ability to pay for healthcare services" was very successful in Korea due to solidarity. The concept was quickly accepted in Korea, while in communities with an emphasis on individualism, like Latin America countries, such a concept was unadoptable (26). Although Vietnam is not a homogeneous country, solidarity has been a crucial social value in developing socialism in Vietnam. Moreover, having an agriculture culture for a long time in history, the risk-sharing concept is largely acknowledged as the power of the nation.

Similarities: political leadership

Political leadership has been a key factor in developing health insurance by pushing political legitimization, mobilization of resources, and decision-making. Taking power through a coup d'etat in 1961, the Korean military administration was forced to develop social security system to stabilize domestic affairs and compete with its rival North Korea, who was developing socialism. The government established a sufficient legal framework and mobilized capable technocrats to develop and implement health insurance policy. With a strong political will, a top-down approach was implemented oppressing some key interest group such as medical providers (22).

Vietnam has only one political party, the communist party, which is the ruling party. Vietnam is one of few countries following socialism, in which a social safety net is always of top priority. More than once, the government of Vietnam has expressed the attempt to achieve universal coverage of health insurance. Therefore, Vietnam and Korea share the political motivation as well as the political environment of not having an opposing political party while developing health insurance.

Differences: distribution of population

Urban areas with better infrastructure and higher density of healthcare facilities make the operation of health insurance more well-organized and well-managed (20). During the 1960s, the urban population in Korea accounted for 30% of the whole population and quickly increased to 50% in the 1970s and to 70% in the 1980s. The baby boom period in Korea occurred in the late 1960s and resulted in a plentiful of labor force for the country by the late 1980s. The speed of industrialization and urbanization in Vietnam is slower than that of Korea, with a rural population of 78% in 1994 and 70% in 2009 (27). However, Vietnam has larger proportion of eligible workers contributing health insurance through wages, which ensures stable revenue for health insurance. In 2009, an amount of 20.3% of Vietnamese population was salary workers (28) while this number was 15.5% in Korea in 1988 (30).

Differences: structure of the economy

Covering the informal sector population has always been a challenge to any national health insurance system (20), therefore, a larger portion of the formal sector is desirable to enlarge coverage and collect contributions. In line with the development of health insurance, the labor force of Korea also kept increasing enormously from 50% of the population in the 1960s to 60% in 1977 and 70% in the 1990. The portion of the informal economic sector dramatically decreased from 60% in the 1960s to 42% in 1977 and 20% in 1990.

Vietnam has a rich source of labor with 74.5% of the population in 2009 between ages 16 and 60 yr (28). The portion of wage employment increased from 19% in 1998 to 33.4% in 2009 (28). Industrialization has decreased the share of employment in the agriculture sector from 70% in 1996 to 47.6% in 2009 and increased the share in the industrial and service sectors from 11.2% in 1990 to 52.4% in 2009 (28). Each year the labor market creates an additional 1.5 million formal sector jobs in the industry and service sectors. Although the structural changes in of the Vietnamese economy are slower than that of Korea, a similar trend is observed.

In summary, Vietnam poses sufficient internal forces (economic, politics, cultural, and social factors) to pursue national health insurance typology. What Vietnam needs at the moment is a suitable strategy, which should be referred to the experience of Korea as the country posed many similar conditions with Vietnam when developing national health insurance.

LESSONS LEARNED FROM A COMPARATIVE PERSPECTIVE

Mandatory enrollment and active social marketing

The failure of voluntary health insurance in Korea suggests that Vietnam needs a mandatory enrollment strategy. The current voluntary scheme of health insurance in Vietnam should be substituted by a mandatory scheme to achieve universal coverage and avoid adverse selection (15, 30). Apart from being legitimated by law, voluntary agreement among the population is of no less importance. Therefore, the government of Vietnam put "social marketing" as the top priority. Currently, "social marketing" strategy in Vietnam is passive, whereas insurers stay in the office and wait for citizens to come to them. Therefore, many people do not know where to go to register and how to pay for contributions. On the contrary, Korea implemented an active social marketing strategy in which health insurance agents visited each household to introduce the benefit of being insured and the process of enrollment. Mass media was effectively utilized with advertisement, public debate, and even soft dramas to encourage enrollment.

Unit of eligibility

Enrollment in Korea is on family-based with a generous scope of dependents. Accordingly, any family members who produce no income are eligible regardless of places of residency within the territory (31, 32). Therefore, in a short period of time, a large number of people (almost 34% of the population) in the informal sector were insured through this channel. In the context of the high informal sector in Vietnam, a more expanded unit of eligibility would help expand the population coverage in a timely manner as well as reduce fragmentation.

Design of contribution and benefit scheme

One of the main barriers of achieving universal coverage in Vietnam is the limited affordability of a large portion of the population to health insurance contribution. Contribution for salary workers is shared between employers and employees; however, contributions for the independents are fully on the burden of the workers. Contribution for non-worker is individually fixed at 4.5% of minimum salary of the civil servant regardless of the living location (rural or urban), and economic status (rich or poor). This imposes an unequal contribution burden and makes health insurance expensive, especially to the near-poor. On the contrary, contribution in Korea is designed on family basis under the principle of ability-to-pay based on income for salary workers and income and asset evaluation for non-workers. Dependents pay no additional contribution. Asset evaluation is calculated on income (taxed-income) and property (house, car, etc.). However, with a non-computerized administrative infrastructure like Vietnam, the design of contribution for the informal sector of Korea is too complicated to apply. Rather the payroll bracket system of Taiwan would be more applicable to Vietnam.

Although expanding the benefit coverage is one of the priorities of the government of Vietnam, a selection must be made between coverage and benefit. Prioritizing the extension of population coverage, Korea traded-off low benefit for larger population coverage even though there have been negative consequences of high out-of-pocket payment and low financial protection on health care (33). On the other hand, the United States chose benefit over coverage by implementing a two-tier system. As a result, one group is over benefited while the other receives no benefits. However, if coverage is chosen, there is still an opportunity to expand benefit for the insured after the achievement of universal coverage.

Resource allocation to National health insurance

More resources should be allocated to ensure the stability of universal coverage to reduce the financial burden of subsiding contribution for more than half of the population of the government of Vietnam. Mongolia achieved 95% of population coverage of health insurance in 1996 but experienced a shrinking trend of population coverage because of financial instability (34). To allocate resources, Korea raised sin taxes of tobacco and alcohol and transferred the money to the health insurance fund. This financial transfer accounted for 3.1% of health insurance revenue in Korea in 2010.

DISCUSSION

In case, if Vietnam decides to focus on population coverage, the government should acknowledge that low contribution and low benefits would be effective only at the starting stage. Prolonging low contribution would cause adverse effects of financial instability and low financial protection. Korea induced low contribution rate since 1977 to encourage enrollment, however passive adjustment of the contribution has failed to catch up with the larger and larger amount of service utilization, resulting in an 18% deficit in the 2002 annual budget and 3% in 2010. The contribution is adjusted based on the performance of the health insurance fund of the previous year which is largely decided by the rate of service utilization rather than the expansion of the benefit coverage. As a result, for the last 30 yr, the contribution in Korea has annual gradually increased while it takes years for benefit coverage to be enlarged modestly. Also, changes in the benefit have not met the expectation of the insured when paying a higher contribution (35, 36). Consequently, only 49.2% of the insured are satisfied with their benefits and 48.4% are satisfied with their insurance contribution levels (37).

The government of Vietnam is fully or partially subsidizing health insurance contributions for 58.2% of the population, meaning that and expansion of the benefit coverage would result in higher financial burden for the government, which could potentially cause financial instability for the health insurance fund. To avoid the financial and structural problems experienced in Korea, Vietnam may consider a contribution co-sharing mechanism between the government and the insured. Accordingly, the government would continue to subsidize for those having no ability to pay while those who can afford health insurance eventually should pay for their contributions. However, it is important to have the citizen recognized that better benefits would deserve higher contribution.

CONCLUSION

This paper contributes to the critical understanding of the challenges and the conditions of Vietnam to achieve universal coverage of health insurance. Results of the comparison study reveals that Vietnam poses significant facilitating factors (economic, demographic, social, cultural, and political factors) to speed-up population coverage. Sharing many similar facilitating factors, it would be preferable for Vietnam to refer to the experience of Korea in order to fully utilize those potential factors. Therefore, the paper addresses applicable lessons for Vietnam from the success and challenges of Korea: mandatory enrollment and active social marketing, unit of eligibility, design of contribution and benefit scheme, and resource allocation. More importantly, from the failure of Korea, Vietnam should learn that the strategy of "low contribution and low benefit" only works at the early stage of universal coverage. On the other hand, this strategy would potentially reduce financial protection and satisfaction of the insured. Additionally, the story of Vietnam on health insurance would serve as a meaningful reference for other developing countries, who are also implementing to achieve universal coverage of health insurance.

XML Download

XML Download