PDF

PDF ePub

ePub Citation

Citation Print

Print

INTRODUCTION

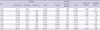

National Health Insurance (NHI) of Korea is facing the risk of financial instability. NHI ran a deficit in 2010 that reduced its cumulative balance to less than 1 trillion Won, or only 3% of the annual budget (1). Unfortunately, this phenomenon was also seen in 2002 when the cumulative balance was negative 2.6 trillion Won, which exceeded the NHI budget by over 18% (Table 1). Another issue facing NHI is that of under-insured benefit coverage, as indicated by public expenditure being 55.3% of the total health expenditure. Only 49.2% of those insured were satisfied with their benefits coverage and 48.4% with their insurance premium levels (2).

NHI's sustainability problem is expected to worsen due to the continuing low birth rate (total fertility rate: 1.22, 2010), aging population (current and projected proportion of population 65 yr and older: 11.3%, 2010; 14%, 2018; 20%, 2026), low economic growth rate (0.2%, 2010), and the potential for Korean unification. While a decrease in funding to NHI is projected, the increasing spending trend appears inevitable.

We conducted a review of the state of NHI with a focus on sustainability, and suggest the directions for the sustainability of NHI in aspects of operating system, funding and spending.

CURRENT STATE OF KOREAN NATIONAL HEALTH INSURANCE

NHI has had its ups and downs. On the upside, it took a very short time, namely just 12 yr from 1977 to 1989, to establish coverage for the whole Korean population. Waiting times for various medical diagnoses and treatments are very short, and the quality of medical care is good (3). In addition, all NHI claims data are in electronic form. However, NHI has downsides, as well. Even if all Koreans are covered with NHI or Medical Aid, public expenditure as a proportion of total health expenditure is only 55.3%, compared to an average 72.5% among member countries of the Organisation for Economic Co-operation and Development (OECD) (Table 2). The proportion of households with catastrophic medical spending is about 2%, which is the highest among OECD countries (4). Also, only 49.2% of those insured report being satisfied with NHI (2).

One of the reasons for these phenomena is a low contribution rate to NHI (5.64% of payroll income, 2011). This low contribution rate, which was induced from low economic level, US $1,000 per capita GDP in 1977 when NHI started, has been maintained until now. This has resulted in under-insured (low benefit coverage) and low level of medical fee schedule leading that healthcare providers have been developing non-covered services (5). Thus, the out-of-pocket expenses of individual beneficiaries have increased in spite of some efforts of expanding benefit coverage from the government, and the medical practice patterns is distorted because of the disproportionate expansion of non-covered services. This has created dissatisfaction with the NHI and medical care (Fig. 1).

Before the initiation of NHI in July 1977, Medical Aid for the poor was introduced in January 1977. The idea was to provide urgently needed medical care security for the poor with the adoption of Medical Aid. However, the dual system of National Health Insurance and Medical Aid has persisted long after the establishment of universal NHI in 1989. While 2010 spending per NHI (20% co-insurance program) enrollee was 809 thousand Won, spending on those covered by Medical Aid Type 1 (no cost sharing program) and Type 2 (15% co-insurance program) was 4,669 thousand and 1,340 thousand Won, respectively. Even taking into account the less healthy and older Medical Aid Type 1 enrollees, the difference is big enough to presume that some Medical Aid Type 1 users may be abusing the program, that is, committing significant extent of moral hazard.

RISK FACTORS OF SUSTAINABILITY OF NATIONAL HEALTH INSURANCE

As of 2011, NHI is in an unhealthy financial state, and 3 main factors threaten its sustainability. Firstly, we are in an era of low birth rates, an aging population, and low economic growth rates. The low birth rate issue could possibly culminate into reduced funding for NHI. Low economic growth also threatens funding to NHI as the contribution rate is tied to the income of the beneficiaries. Additionally, the world's most rapidly aging population is found in Korea, which will inevitably be a burden to overall healthcare costs.

Secondly, the expected unification of South and North Korea would be a challenging factor for NHI. Although the exact timing and method of unification cannot be predicted, the burden of unification is inevitable. Population size is of great concern: South and North Korea have populations of 48.6 and 23.3 million, respectively, whereas the respective populations of West and East Germany were 62.0 and 16.6 million at the time of unification (1990). Therefore, the per capita burden in the case of Korean unification is much greater than what it was for German unification. Furthermore, the present economic situation on both sides of Korea (per capita GDP, 2010: South US$ 19,105; North US$ 1,060) is worse than that of both East and West Germany (per capita GDP, 1990: West 19,283; East 5,840). Unification is thus a critical factor in examining the financial sustainability of NHI.

Thirdly, political campaigners frequently bring up the issue of health security. Past election pledges spoke of economic issues, but at present health and welfare issues are of greater concern. The opposition party advocates that the level of benefit coverage for hospitalization should be raised to 90%, from the present level of 60%, and they accordingly project a budget of 8.1 trillion Won. However, considering the potential for moral hazard, budgets ranging from 12.7 to 35.1 trillion Won (price elasticity -0.25 to -1.0) could be expected. The benefit expansion as a result of political campaigning appears to increase the risk of financial unsustainablility for NHI.

DIRECTIONS FOR NATIONAL HEALTH INSURANCE FOR SUSTAINABILITY

Below we describe some suggested directions for NHI in terms of their operating system, funding, and spending. With respect to their operating system, the integration of NHI and Medical Aid should be considered. The high spending by Medical Aid Type 1 must be controlled, and there are some disparities with low income NHI beneficiaries who are just over to Medical Aid enrollee. Integration would solve these problems by implementing the same controlling mechanism for Medical Aid, the same as that of NHI, and by using a sliding benefit coverage system to income's level of NHI. This could reduce the cut-off phenomenon that occurs between Medical Aid and the lower income group in NHI.

NHI as a single insurer should introduce an internal market and create a competitive environment within its regional organizations. This would increase the efficiency of NHI and also allow implementation of various benefit packages and operating systems by regional insurers. We suggest that a central insurer collect the funding as is currently done and distribute the risk-adjusted funds to regional insurers.

NHI should work closely with the Medical Cost Supporting System (MCSS) for low income groups, and function as medical security system with MCSS. The close connection between NHI and MCSS will reduce the number of households with catastrophic medical costs with relatively small funds comparing to expansion of benefit package for all.

The directions with respect to NHI funding are to increase the contribution rate and expand the funding sources for NHI's contributions. The contribution rate, which is 5.6% in 2011, could increase with agreement from the beneficiaries, which is not easy but is tried continuously. Funding sources could expand to include financial income, rental income, pension, as well as payroll income. The expanding funding sources would increase the equity of contributions: an industrial worker's contribution would be calculated based only on payroll income, but the contribution of self-employed would be based on both income and property. Also, the reserved funds must be accumulated least 50% of the annual budget, as described in the article 36 of the National Health Insurance Act, but the reserved funds of NHI at 2011 only 3% of the annual budget. In company with complying the Law, we insist on expanding the reserved funds of NHI to 100% of the annual budget for Korean unification.

With respect to the spending side of NHI, the benefits package would be reformed to increase coverage for large medical care costs and reduce coverage for small medical care costs (6). Coverage of large medical care costs would be expanded by using a prioritized list based on medical effectiveness, not by service items (7). For small medical care costs, NHI would consider a medical savings account and deductible as a cost-sharing method, as the number of physician office visits is much larger in Korea than among OECD countries (1). Moral hazard could thus be reduced by using a medical savings account and deductible program. Cost recognition on the demand side is needed in the present situation. A payment system change to include aggregated payment units (Diagnosis-Related Groups, Diagnosis-Treatment Combinations, and global contracting systems) also should be considered to raise cost recognition among providers. A barrier to that change, however, is the low level of NHI's fee schedule which is 70%-80% of costs in covered services. In addition to these changes, pay for performance (P4P) should be introduced. A demonstration project of P4P on inpatient care for acute myocardial infarction and cesarean section should be evaluated and extended to outpatient care as soon as possible. Various new information and communication technology of medical care could be experimented with the institutional provision. The enrollee's profiling is needed for controlling moral hazard.

Conclusively, for the sustainability of NHI, new paradigm is needed that is proper contribution - adequate benefit coverage - fair NHI's fee schedule with reforming in operating system, funding and spending.

XML Download

XML Download