PDF

PDF ePub

ePub Citation

Citation Print

Print

INTRODUCTION

The population in Korea is rapidly aging; the proportion of people aged 65 yr and older increased from 7.2% in 2000 to 11% in 2010 (1). According to an official prediction based on the population dynamics of fertility and mortality, 14.5% of Koreans will be over the age of 65 in 2018, increasing to 20.8% by 2026. The economic and psychosocial burden imposed on older adults and their caregivers is increasingly being recognized as a major social problem, with wide political implications, given the rapid increase in the Korean elderly population.

Against this challenge, the Korean government implemented mandatory public long-term care insurance for older adults on August 1, 2008. The purpose of the Long-Term Care Insurance (LTCI) is to preserve and improve the quality of senior citizens' and their caregivers' lives, promote better health and stable livelihoods, and reduce the burden of care on family members. The elderly aged 65 yr and older or persons less than 65 who have geriatric diseases are eligible for benefits through an assessment process certifying the presence of disability in physical and cognitive functioning. LTCI benefits include institutional as well as community-based services. The level of certification determines the amount of services covered and the fee for each service. Seniors with certified needs can use covered services from public and private providers based on their preference.

Despite its early adoption and introduction of novel services for older people, LTCI has often been criticized for failing to take into account the healthcare needs of older beneficiaries because of its emphasis on the provision of social and support services. Establishment of a separate scheme from the national health insurance program has further engendered difficulties in the coordination between healthcare and long-term care services (2). Delivery of healthcare in long-term care settings has consequently been fragmented and unorganized.

In this paper, we introduce the key components of the Korean LTCI system by presenting an overview of its operation involving the certification process, benefits and coverage, and financing. Healthcare needs of long-term care beneficiaries are then examined by analyzing their health and functional status and healthcare use. Challenges both unique to the Korean LTCI and shared among countries with a public LTCI are discussed in the context of addressing the healthcare needs of older beneficiaries navigating through the complex long-term care environment.

ELIGIBILITY & ASSESSMENT

Eligibility for services under the LTCI program is determined by the older person's physical and mental status, irrespective of their financial status or family support. To use services covered by the LTCI, the elderly person or his/her caregiver has to contact the National Health Insurance Corporation (NHIC) to have the applicant's care needs officially certified. To evaluate the applicant's care needs, well-trained assessors in the local branch of the NHIC visit the applicant's home and interview the applicant or his/her primary caregivers. Primary caregivers have often been shown to be accurate reporters of medical and social information of the elderly (3). A structured questionnaire about physical and mental status is used in all interviews. This questionnaire includes the government-certified disability index (4, 5), a 52-item assessment instrument containing 5 domains of function and conditions (Table 1).

Results of the assessment are entered into the computer to calculate the applicant's standardized scores for the five domains, for which activities of daily living (ADLs) have been found to contribute significantly to the overall score. These scores are then used to estimate the service time, with a care need level assigned based on the total estimated time. The computerized needs assessment system categorizes people into six levels of care need.

Each local branch of the Long-Term Care Center, under the jurisdiction of the NHIC, operates the Needs Assessment Committee, consisting of physicians, nurses, and other experts in health and social services. The Needs Assessment Committee reviews the assigned scores of the applicant, taking into account the medical statement of the primary care physician and specified comments by the assessors. If necessary, the committee can reassign the levels of care need. Usually the committee upgrades the care level in consideration of special needs not captured in the computer-based assessment. The applicant who is determined to be in care levels 1 through 3 - level 1 being the most severely disabled - will be eligible to receive LTC benefits.

BENEFICIARIES, BENEFITS, AND FINANCING

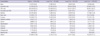

The number of people applying for long-term care certification was 402,815 persons in 2009. Among them, 286,907 (71.2%) were assigned to levels 1, 2, and 3 (Table 2). More than half of those certified to receive benefits were in Level 3, and 70.7% were women.

The type of long-term care benefits consists of community-based home care and institutional care. Home care includes home-visit care, home-visit bathing, home-visit nursing, day/night care, and short-term respite care. For example, home-visit care includes physical support and household work provided by trained personnel in the beneficiary's home. Institutional care includes services provided to beneficiaries admitted to long-term care facilities for the elderly (excluding geriatric hospitals), with nursing care and assistance to maintain and enhance physical or mental functions.

Long-term care benefits are provided in an amount that is subject to a monthly limit. Monthly limits are calculated according to the care need levels and type of benefits provided. The beneficiary can use more services than covered as long as one pays all the costs for the services beyond the maximum level. Table 3 shows the monthly limit and service benefits of LTCI by each care level. Institutional benefits are per diem. Per diem rates depend on the person's care need level and the type of facility. Services are paid for with 15%-20% co-payment, and the remainder is paid for by premiums. The total expenditure of LTCI was 1.7 trillion won (about 1.5 billion dollars, $US 1 = KRW 1,125) in 2009. Of the total expenditure, 56% was for home care benefits and 43% for institutional care (6).

LTCI is financed by contributions from premiums, user copayments, and government subsidies. The Minister for Health and Welfare is in charge of the insurance scheme. The insurer for the LTCI is the National Health Insurance Corporation (NHIC). The NHIC collects long-term care insurance premiums to finance the costs. The LTCI premium is linked to the health insurance premium of the National Health Insurance, set at a specified rate under the LTCI Act.

HEALTHCARE NEEDS OF LONG-TERM CARE BENEFICIARIES

Functional status of LTC beneficiaries

While Korea has a universal health insurance system, the newly introduced LTCI is an elective beneficial coverage. This means that beneficiaries of the LTCI are also eligible for health insurance. Those who have reduced functional status due to geriatric conditions or related problems and need physical support or assistance for household works receive medical services through the national health insurance system (7).

Table 4 indicates the functional status of long-term care insurance beneficiaries from April 2006 to April 2007, during which the demonstration program to introduce the long-term care system was in operation (8). On average, the beneficiaries' functional status was worse than the applicants. The average score of ADLs among the applicants was 15.1 and that of the beneficiaries was 23.8. Overall, those in Level 1 appear to have more problems with functioning than those in Levels 2 or 3.

Healthcare use of LTC beneficiaries

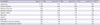

Healthcare needs among long-term care beneficiaries may be inferred indirectly from data on their healthcare utilization. Table 6 shows diagnosed comorbidities of LTCI beneficiaries using National Health Insurance claims data (8). Of the LTCI beneficiaries, 2,006 (25.9%) used medical services for hypertension in 2006. Hypertension, cerebral infarction, arthrosis of the knee, and dementia were common conditions requiring health services.

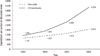

Fig. 1 exhibits the 4-yr trend in healthcare expenditure by those who were certified as beneficiaries in 2006. The beneficiaries spent, on average, 4.3 million won per person in 2006, almost double the amount (2.8 million won) expended in the previous year and a steep rise from the 1.4 million won spent in 2003 (9).

During this period, the number of individuals comprising the older population has rapidly grown, with older adults using a disproportionate amount of medical services due to high morbidity. Moreover, advances in health technology have contributed to the increase in healthcare costs. LTCI beneficiaries, compared with the total older population, used more medical services and demonstrated a higher rate of increase in healthcare costs. This was especially prominent for inpatient services.

CHALLENGES IN DELIVERING HEALTHCARE IN LONG-TERM CARE SETTINGS

Chronic diseases dominate the morbidity pattern of the elderly (10). They develop slowly at first, then progress and become clinically evident once a certain symptomatic threshold has been reached, usually quite late in life. The presence of multiple chronic conditions, quite common in older people, increases their risk of developing disability and dependence (10, 11). The elderly often have concomitant needs for both healthcare and long-term care (7).

Traditionally, medical care for the elderly was provided by hospitals, but a more complex picture has evolved with the development of an array of medical and social services over the years (12). Long-term care facilities have emerged that accommodate older adults who are not only disabled but also have a number of chronic conditions. In Korea, 92% of long-term care beneficiaries suffer from chronic diseases, and 74.2% of them utilize medical services (8). In spite of entering into the long-term care system, the need for disease management of these beneficiaries is not diminished (13). One of the challenges of the present health and long-term care insurance program is how to meet the complex medical needs of those residing in long-term care facilities or using community long-term care services.

In principle, health insurance is designed to provide medical services benefits, whereas long-term care insurance provides for care services that go beyond acute medical needs to include social services and personal support. However, it is difficult to distinguish between the two needs in older people because they often exhibit needs that require both health and long-term care simultaneously. As older people's needs for both health and long-term care increase, excessive or even redundant use and provision of services may arise due to the current disconnection between the two systems. Moreover, the disabled elderly may not be able to identify and express their needs explicitly such that selection of and linkage with the appropriate combination of health and long-term care services may not be feasible. It is, therefore, important to construct an integrated delivery system that provides coordination between long-term and healthcare services (7). An efficient integrated system would require that appropriate services are matched according to the older person's health and functional status.

The first stage in which healthcare's role comes into play in long-term care is in determining eligibility and designating care levels of the beneficiary. During the formal review process by the Needs Assessment Committee, the physician's statement about the individual patient's health conditions is considered. This is to ensure that complex medical conditions of the applicant are accurately reflected in the review process with proper designation of the care level needed by the long term care beneficiary. The physician's statement can be issued by practicing physicians in either western or Korean traditional medicine and is not limited to a certain specialty (Enforcement Decree for the Act on Long-Term Care Insurance for Senior Citizens, Article 2). There remains, however, some doubt as to the proper functioning of the physician's statement in the designation of beneficiaries' care levels. Physicians are not satisfied with the reimbursement for their assessment and are suspicious of the long-term care system, regarding it as a separate entity initially created to exclude active physician involvement. These have, in part, also resulted in long-term care applicants' dissatisfaction with the certification process.

Healthcare plays an essential role in several aspects of the delivery of long-term care services. First, among the community long-term care services, home-visit nursing service involves active medical care. Nurses provide home-visit nursing care services under the direction of the physician. It is, however, often difficult to obtain the physician's instructions for home-visit nursing care in cases where the physician is not affiliated with the provider or is hired on a contract basis. Home-visit nursing remains the least utilized service among the community long-term care services. This is in part due to the lack of a systematic assessment of the need for home-visit nursing care of the beneficiary. Moreover, although the individual patient's current health status is noted in the physician's statement for long-term care applicants, the type and amount of prescribed or recommended medical and nursing care are not specified.

Second, there are contracted physicians in long-term care facilities. This system was in place even before the introduction of the LTCI. Contracted physicians, however, are usually not able to properly manage the elderly in long-term care facilities because of their duty at their affiliated hospitals or clinics. Moreover, no economic incentives are available for the hospital or clinics in having physicians who contract out their time to long-term care.

Third, a cooperative agreement between medical and long-term care institutions was introduced to complement the problems with contracted physicians. Because long-term care facilities have difficulty acquiring an adequate physician workforce, long-term care facilities have forged formal collaborative ties with local hospitals. This has facilitated residents in long-term care facilities to seek consultations from physicians in other hospitals. Satisfaction with these services, however, is not high. In a survey of long-term care facilities, 31.1% of providers were not satisfied with the level of cooperation with hospitals, and 36.9% viewed management of medical conditions as being inadequate (14).

One of major organizational barriers in linking services between long-term care and healthcare is the indistinct role between geriatric hospitals and long-term care facilities (nursing homes). Over the past decade, there has been a steep rise in the number of geriatric hospitals, also known as long-term care hospitals. These provide inpatient chronic care and rehabilitative services for geriatric patients who have conditions such as stroke and dementia. Geriatric hospitals are managed through the national health insurance system, while long-term care facilities operate under the LTCI. The unclear role between the two institutions is manifested in their similar patient composition, with dementia and stroke being the most prevalent conditions (14). A study on geriatric hospitals and long-term care facilities has revealed that 38.6% of patients in geriatric hospitals would be better served in long-term care facilities, whereas 13.9% of long-term care facility residents should be admitted to geriatric hospitals (15). This shows the inadequacy in the functional division between the two institutions and an inefficient use of care resources. Over time, the inappropriate utilization behavior of older people may have a negative impact on the financing of the two insurance systems. It is important to establish a clear role and delineate the function of the two institutions by developing an appropriate payment and delivery system (13).

Healthcare professionals may play a vital role in guiding older people to use appropriate health and long-term care services. The personal physician may serve to assess the patient's health status and direct the coordination of services to meet the older person's various care needs. Nurses and social workers can then provide and link specific services according to the individual person's needs. Working as a team, healthcare providers can use their professional expertise to guide the older patient through the maze of the long-term care system to receive quality healthcare (16, 17). Provision of effective and efficient delivery of comprehensive health services to older people in the evolving long-term care environment would require an active participation on the part of healthcare professionals.

CONCLUSION

Older long-term care beneficiaries have complex healthcare needs that make delivery of long-term care services particularly challenging. The lack of coordination between health and long-term care services, inadequate consideration of physician's assessments in the LTCI certification process, insufficient provision of health services in long-term care facilities, and overlapping and inefficient use of health and long-term care resources, further, act as barriers. Healthcare professionals need to take a more active role in guiding older patients navigate through the long-term care terrain to access appropriate health services.

XML Download

XML Download